.avif)

Fundraising is challenging, we get it. Beyond the pitch and the outreach, there’s still a fundamental gap between founders and VCs. At Forum Ventures, we've worked with 550+ portfolio companies and 1,000+ founders since 2014. We’ve learned that what many founders lack is the right mental model for approaching VCs.

The fact is that most people don’t even know how early stage investors make decisions. What are their incentives? How do VCs actually work behind the scenes?

To win investors, it’s best to first understand them. Speak their language, understand their goals, and align your fundraising strategy to start closing term sheets.

"Most founders walk into investor meetings thinking they need to prove their idea works. What they actually need to prove is that it can return a fund." — Michael Cardamone, CEO & Managing Partner, Forum Ventures

This post covers lessons from Sruthi Sivanandan, Investment Analyst at Forum Ventures, from the first part of a Health Tech Masterclass series hosted by Mt Sinai Innovation Partners in April 2026. The session focused on venture capital math and the real driving forces behind investor decisions.

A fund is a fixed pool of money with a hard deadline

A venture fund, at its core, is a pool of money with a hard deadline. A VC firm raises money from Limited Partners (LPs), which commonly include pension funds, high net worth individuals, and university endowments.

These LPs will commit capital just one time at the fund’s inception, after which they’ll wait for 7-10 years to get returns.

The VC fund has roughly 3 to 4 years to deploy all that capital, and the total fund has around 10 years to return meaningful profit to the LPs.

What does this mean? VCs can’t simply hold an investment for 15 or 20 years to see what happens and enjoy long-term growth. There is a tangible deadline at year 10 with an obligation to achieve returns to LPs.

This is why VCs care so much about high growth and traction. It’s not just a matter of whether you can become a successful business. It’s whether you can grow your valuations fast enough for your VCs.

From a fundraising perspective, your pitch should make your startup seem like it has potential to grow quickly and become a unicorn before the VC’s deadline. This doesn’t mean outlining an unrealistic growth plan that would make an investor skeptical, but it definitely means to never outline a slow growth pathway, even if it’s consistent.

This is also why some VC firms (especially new ones) require traction even in early stage funding, because companies with traction are more likely to scale their valuations fast enough to meet that 10-year deadline. On an additional note, they can grow faster and more successfully even within 1-2 years. This allows the VC firm to show LPs high TVPI, or total value to paid in capital, the realized and unrealized gains the VC generates compared to their initial investment.

With this context, know that if a VC feels like they’re pushing you towards certain decisions that feel premature to you, it’s often because their clock is running.

What is Power Law?

Most VC investments do not return anything at all. Out of hundreds of companies, the entire fund’s returns come from a small minority of successful investments (e.g. 3 unicorns out of 100 failed startups). This is what we call Power Law.

These few companies generate 10X to 1000X returns of their initial investment, covering the losses the VC has from all their other investments.

As a result, VCs need to aim high. Even if a business seems viable and profitable, if it doesn’t have potential to become a $1B company, a VC would not invest in it.

As a founder, your goal in your pitch is to convince the VC that you have potential. You don’t have to prove that you’re extremely likely to become the next Steve Jobs; VCs already know and expect that to be unlikely from their perspective. They just want to see a potential pathway that’s worth betting on, because out of hundreds of similar bets, one will actually come true.

When you hear investors ask “how big can this get” or “how big is this market”, this is exactly what they’re looking for. They’re asking to figure out if your company can be those one or two exceptional investments in their portfolio.

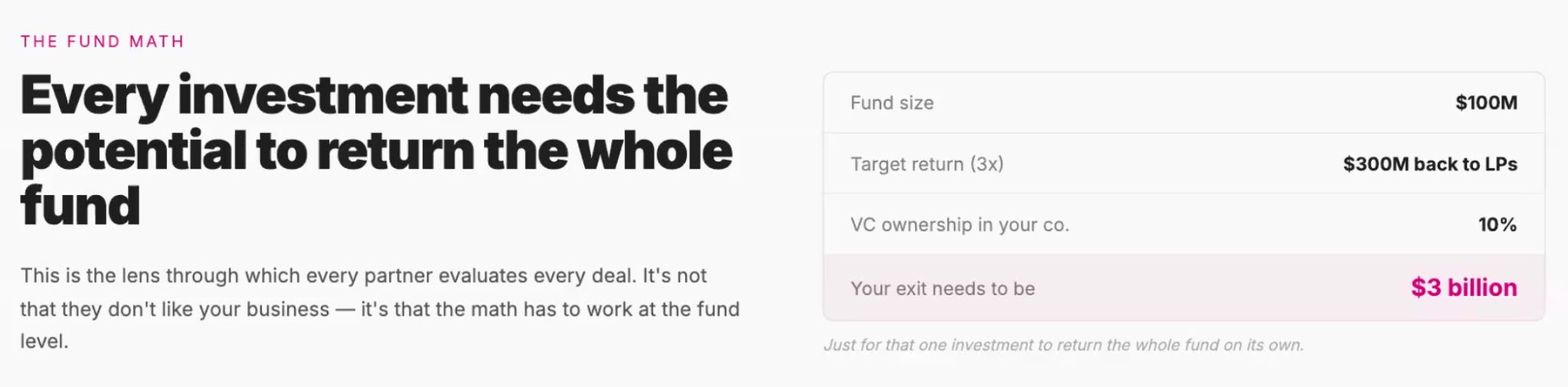

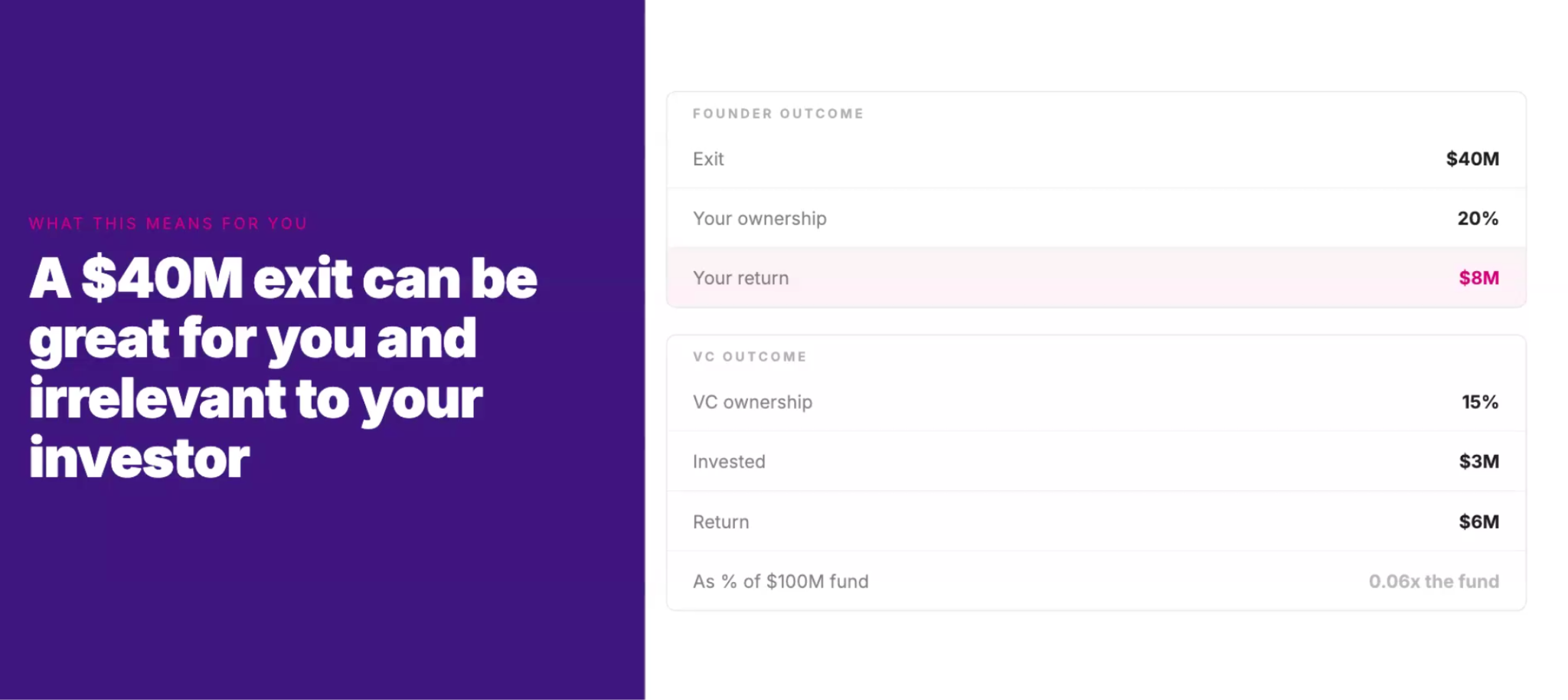

What does power law look like in real numbers? In the above example, you’ll see that for the VC to return profits to LPs at their target return, your company would need to become worth $3 billion (not even accounting for dilution).

So when a VC is telling you that they don’t think the market is big enough, it means that even if you’re on your way to a $50M business, it’s simply not the outcome what the VC needs.

The exit might be life changing for you as the founder, but the returns to a VC is barely a baby step towards their goal. This is why there’s many cases of acquisition offers where the founder wants to take the deal (because it’s lucrative enough for the founder), but the VC does not (because it’s far from being enough for the VC).

In 2026, Forum portfolio company Fireflies.ai crossed a $1 billion valuation, a good example of a big outcome VCs are interested in.

The takeaway is before you sign that term sheet and enter into a multi-year relationship with the VC, have a serious conversation about what success means for both of you. You might be looking for a multi-million dollar recurring business, but the VC is looking for you to keep growing the company to a billion dollar valuation. That misalignment could cost you down the line if you don’t set expectations early.

Here’s another helpful guide on what VCs look for in the early stage: https://www.forumvc.com/thought-pieces/what-vcs-look-for-early-stage-investment

Ownership percentage is everything to a VC

VC ownership percentage gets diluted when other investors join the company. In exchange for capital, an investor typically receives a fixed amount of common or preferred shares. When the company welcomes another investor, they issue completely new shares to that investor.

Suppose you initially owned 10 shares out of 100 total shares (10% of the company). The company then issues 100 more shares to a new investor, bringing the total shares amount to 200. Your ownership has effectively gone down to 5%.

This is what we call dilution.

Let’s apply this concept to a hypothetical future exit that is worth $500 million. Suppose the VC is set to own $75 million from its 15% ownership at the preseed stage.

However, as more investors come in, by the time the company is in Series A, the VC might only have 8% ownership, bringing their total value down to $40 million. This is a massive gap in returns.

So when investors push back on your valuation, ask for pro-rata rights, or negotiate for some sort of anti-dilution protection, it traces back to this core concern.

Pro-rata rights are contractual provisions allowing investors to maintain their ownership percentage in a company by participating in future rounds. This grants investors the option, not an obligation, to purchase a certain percentage of a future round. This effectively protects the investors from dilution.

It’s no longer a “grow at all costs” game.

After 2022, the “grow at all costs” mentality toward startups was largely dismantled. Companies used to burn as much cash as possible to achieve growth, despite being inefficient or unprofitable.

However, this methodology is no longer attracting VC investors in the same way. In 2026, the market has stopped rewarding this behavior, and investors are increasingly concerned with unit economics, margins, and a path to profitability.

Questions like who are you hiring and how you are going to find the balance between growth and profitability are now important considerations for VCs. The way you burn cash and manage cash flows can also make or break your fundraise.

Regardless of this shift, at its core, VCs still want to see proof that you can become one of their big outcomes.

The bottom line is that in addition to showing capital efficiency, you still need to paint a clear picture of high growth. It’s a balance between the two.

What you need to prove to VCs today:

- Large market

- Fast but capital-efficient growth

- A clear path to a large exit

What you need to avoid:

- Pitching a sustainable, profitable, but niche market

- Smaller exits and early exit plans

Making sense of common VC questions

With the above context, we can easily piece together why VCs ask certain questions and make sense of what they’re trying to validate about your startup. Understanding this allows you to practice and build the optimal responses that can alleviate their concerns.

Not every great business is a venture-scale business

Just because your startup doesn’t fit that large market, high efficiency and high growth model, it does not mean you can’t have a great business.

It just means you’re not a venture-scale business.

The question you should be asking yourself is what type of business you’re trying to build, what your personal goals are, and if you even need venture capital funding. For example, if you’re aiming for an early to mid-stage acquisition, you’ll probably be misaligned with venture investors.

Even if you need financing, there are numerous other options such as debt and government grants which could fit your business a lot better. Here are a few more helpful but often underused channels:

- Revenue based financing and revenue sharing models

- Bootstrapping

- Strategic partnerships (co-financing in a joint venture)

If you're weighing your options, read our guide to bootstrapping vs venture capital vs angel investment to figure out which financing model fits your goals.

Venture studios is another up and coming route that’s still within the venture track but with several key differences. In contrast to accelerators, venture studios have an even higher degree of involvement with each startup they invest in. They take higher ownership but help build the company with a full stack early team, rather than just mentor or advise. At Forum’s venture studio, we give founders an entire tech team to build MVPs and a GTM team to land their first customers or design partners.

Because of this higher level of involvement, some studios operate in more niche and highly specific (albeit still large) markets rather than always following a general “hot” trend. Additionally, studios have boasted stronger success rates for startups and a lower risk founder journey. In 2026, Forum Ventures' AI Studio portfolio companies raised follow-on capital within 12 months at a 63% rate, beating the industry's historic average of less than 50% over 18 months.

Venture capital is specifically meant for businesses trying to reach that unicorn status, to dominate a large market, and to grow quickly and efficiently. While it seems to be the most popular form of entrepreneurial success, it’s not always going to be the best option.

Building a $50M business where you own 100% of the profits can be just as lucrative as owning a small portion of a billion dollar business. For instance, Peter Thiel’s exit from PayPal’s $1.5B acquisition was around $55 million. Even though the total valuation is larger, various factors like dilution hampers a founders’ returns.

In fact, in extreme cases like FanDuel, despite the company being sold for $465 million, the founders ended up with virtually nothing due to their terms and preferences to investors.

The bottom line: venture isn’t everything; it’s just a means to an end.

If you want more info on evaluating your term sheet, read our guide to evaluating a post-money SAFE for your B2B AI startup.

Go in with eyes open

When you’re fundraising and a VC question seems odd, consider the context of what we discussed about fund math. Ask yourself: what fund math is driving this question? Is it their ownership percentage or the potential for a massive outcome? The answer is usually there, among the various incentives of the fund.

Secondly, before you take a term sheet, understand what return that fund needs. For example, returns are different between early stage and later stage funds. Make sure that your vision and incentives are compatible with the investor’s, or more problems will come up down the line.

Finally, model your dilution. It’s not just VCs who should be concerned about their ownership; the same applies to you. Know what you’ll own in different exit scenarios, whether that be a late-stage acquisition, Series A or Series B, or even a worse case down round.

At Forum Ventures, we walk founders through these alignment conversations and decisions during the fundraising track of our accelerator and venture studio process – including working through dilution scenarios and investor fit before a raise begins. Our 65% three-year average fund-through rate reflects what that preparation looks like in practice.

Frequently Asked Questions

How do VCs decide which startups to invest in?

VCs invest based on fund math, not just business quality. They need companies that can return the entire fund — typically requiring a potential valuation of $1B or more. They evaluate TAM, growth speed, capital efficiency, and whether the team can execute. A great business that caps out at $50M revenue is not a VC-scale business, even if it's profitable.

What is power law in venture capital?

Power law means that in a VC portfolio, the vast majority of returns come from a tiny number of investments — typically 2 or 3 companies out of 100. Those outliers generate 10x to 1,000x returns and cover all losses from failed bets. This is why VCs only invest in companies with genuine unicorn potential, even if the probability is low.

Why do VCs care so much about TAM?

TAM (total addressable market) determines whether a company can become one of the fund's big outcomes. If the entire market is worth $200M, the company can never reach a $1B valuation — which means it can't meaningfully return a $100M fund. VCs need large markets because they need room for their investments to grow into unicorns.

What is dilution and why do investors worry about it?

Dilution happens when a company issues new shares to a new investor, reducing the ownership percentage of everyone who invested before. A VC who owns 15% at pre-seed might own only 8% by Series A. Since VC returns are calculated as ownership percentage times exit value, dilution directly reduces how much they make — which is why investors negotiate for pro-rata rights and anti-dilution protections.

What are pro-rata rights in venture capital?

Pro-rata rights give an investor the option to invest in future funding rounds to maintain their ownership percentage. If a VC owns 10% and the company raises a new round, pro-rata rights let them buy enough of that round to stay at 10%. This protects their returns against dilution from later investors.

How long does a VC fund have to return money to investors?

A typical VC fund has a 10-year lifespan. LPs commit capital once at inception, and the VC has roughly 3–4 years to deploy it and 10 years total to return profits. This hard deadline is why VCs push for fast growth — a company that grows slowly over 15 years may be a great business but can't return the fund in time.

Is venture capital right for every startup?

No. Venture capital is designed for businesses targeting large markets with the potential to reach $1B+ in value within 10 years. If your goal is a profitable niche business, an early acquisition, or steady growth without massive scale, VC will likely create misaligned incentives. Alternatives like revenue-based financing, bootstrapping, strategic partnerships, or a venture studio model may be a better fit.

What is a venture studio and how is it different from an accelerator?

A venture studio co-builds companies alongside founders from day zero — sometimes before an idea is fully formed. Unlike accelerators which advise and mentor, a studio provides a full team across product, engineering, GTM, and fundraising and invests capital at formation. Forum Ventures' AI Studio, for example, invests $250K at formation and co-builds with founders from the pre-idea stage. In 2026, 63% of Forum AI Studio portfolio companies raised follow-on capital within 12 months of formation, beating the industry average of under 50% over 18 months.

What is TVPI in venture capital?

TVPI stands for Total Value to Paid-In capital. It measures the total value a VC fund has generated — both realised gains from exits and unrealised gains from current portfolio valuations — divided by the capital invested. A TVPI of 2x means the fund has generated twice what was invested. VCs track TVPI to show LPs how the fund is performing before the 10-year deadline.

.svg)

.avif)